Portfolio Update Juli 2021

I want to give a short update and show some statistics regarding my portfolio today. The update already includes the most recent addition, Alpek SA, a Mexican Chemicals company. I want to start out with some historic statistics in comparison to benchmarks. The following chart shows the money-weighted cumulative return in comparison to a custom benchmark consisting of an equal-weight allocation to the 5 Alphaarchitect factor ETFs (AA). I choose Alphaarchitect ETFs as my benchmark because they would be my go-to alternative I can trust (if I had access). Clearly, my portfolio was more volatile, especially during 2020 but my global, concentrated & integrated factor approach apparently played out nicely so far. Of course this is no guarantee that it will continue like this going forward.

To get more detailed stats, I have to switch to time-weighted (TWR) comparison (MWR not supported in the Captrader PortfolioAnalyzer). In the following table, main risk and return parameters are listed in comparison to my AA benchmark, the iShares MSCI ACWI ETF (ACWI) and the iShares Russell 2000 ETF (IWM). My maximum drawdown in TWR terms is less dramatic since I was not fully allocated in the beginning 2020 (luckily). Thus, the next crysis hopefully will be the first one that will REALLY stress-test my allocation strategy. Nevertheless, I hope you’ll allow me to be at least a tiny bit proud of my performance, even though a lot of luck was involved.

In the following atble, you see all my realized positions so far. My Value-Mom-Quality system started out in April 2019 with building a 20 stock portfolio over the course of 1 year. These positions I held for 12 months each. After this first investment cycle, I decided to switch to 6-month holding periods for better momentum capture. The transition is still going on and will be completed in October 2021.

To check my exposures to main factors, I downloaded the Fama-French Data for Developed Markets (incl. US) and performed a factor regression for my portfolio returns from May 2020 to May 2021. The results are shown in the following table. My market beta exposure was approximately 1. Most of the returns are explained by high exposure to small-caps (SMB) and high profitability (RMW). The latter originates mainly from my high exposure to Price-to-FCF, Price-to-OCF and similar multiples. I don’t use pure profitability metrics like ROIC, Gross-Margin etc. but I use Piotrosky F-score which gives additional exposure to RMW. I also don’t use Price-to-Book, which explains my lower exposure to the “Value” factor (HML), even tough there is some overlay with other Value multiples (e.g. P/E is basically a combination of P/B and ROE). The good exposure to the Investment factor (CMA) mainly originates from the usage of Piotrosky F-Score, External Financing and Asset Growth. Unfortunately, there is no FF-Dev data for the Long-term Reversal Factor (LTR) which I use as well.

A big surprise to me is the negative exposure to momentum (MOM), even though I use it directly in my system. Here are some potential explanations:

Momentum is the factor with the highest decay, which means that the information changes quickly and constant rebalancing is “necessary”. The data shown is based on monthly rebalancing. As written earlier, my system was based on 12-month holding periods and is now slowly shifting towards 6-month holding periods. Thus, the large decay could result in reduced average exposure.

I use a pre-screen to reduce the number of stocks in my ranking to cashflow-profitable and earnings-profitable businesses only. As a result, my momentum ranking does not include unprofitable stocks, which had strong momentum over the recent years. The Fama-French data does not make that distinction and thus might include data for names with much higher momentum.

I only use data for Europe-listed stocks. While this gives me access to global companies, it misses many global small-caps, especially in Australia and Asia, which are included in the Fama-French dataset.

The main observation, however: I have no Alpha to offer! And this is fine. My system is factor-based. I just want the most concentrated factor exposure I can get. Significant Alpha would maybe indicate that I do something wrong.

Please note that I have Bitcoin exposure as well, however, including it in the regression results in no significant change in exposure. Maybe, I should subtract any Bitcoin returns/losses from the monthly portfolio gains/losses for future regression analyses.

Let’s now switch to my current portfolio, which can be summarized as follows:

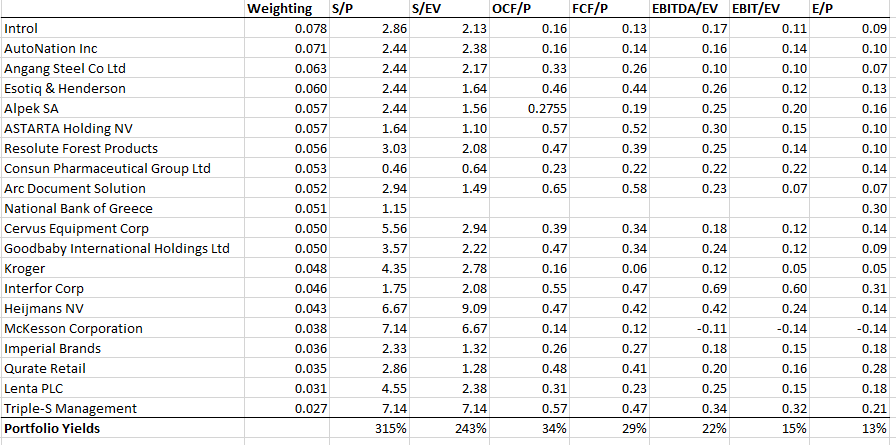

Once again I want to concentrate on the multi-factor portion. I calculated the weightings and the resulting “Yields” of my 20-stock multi-factor portfolio. My portfolio currently has a 12m-trailing FCF-Yield of 29% and an earning yield of 13%. This is much higher than the yield of the MSCI Emerging Markets (5.4% EY) and the MSCI World (3.6% EY). Everyone knows by now that Value spreads across the world are elevated due to the recent Mega-cap Tech boom. The result: High yields for concentrated small-cap value investors.

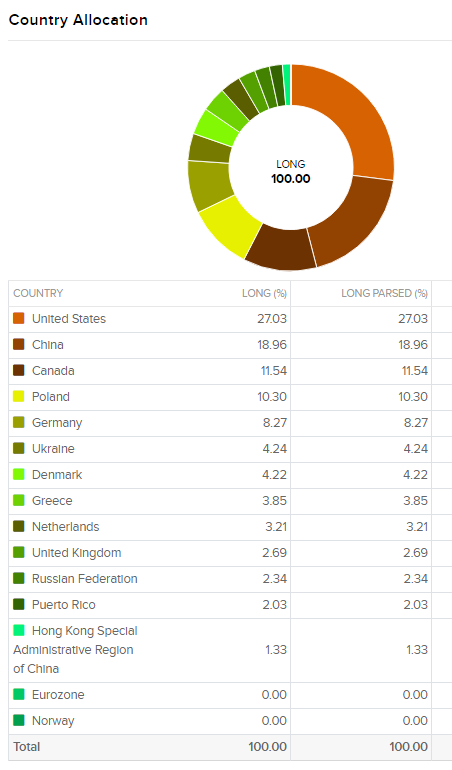

Even though I only have a 20-stock portfolio, I feel rather diversified in the equity space. I have broad exposure to factors but also to regions…

… to countries…

… and to sectors:

For full transparency: I am not really a fan of ESG scores and I do not believe in the fact that small traders in secondary markets have any impact on what’s going on. Nonetheless, I also want to show my latest ESG summary:

To sum up, I am very satisfied with my system so far. Unfortunately, 2020 doesn’t count as a stress-test for me, also because I had personal problems during that time and thinking about my portfolio was the last thing in my mind in March 2020. I am glad that I had a mechanical investing system in place to take the decision-making from me in times of distress but, on the other hand, I don’t know if I would have bailed out under different circumstances. Hopefully, the next crash or pronounced period of under-performance will show me if I can really stick with my investment philosophy. Until then, I will enjoy the good times.

Thanks for reading,

Yours sincerely,

Non-Prophet